Most Accidents Happen On The Way Down

In the late 90’s I and many others were absorbed by Jon Krakauer’s book Into Thin Air that detailed the commercialization of climbing Mount Everest and the lives that were sadly lost in the process. What was really fascinating was how many of these wealthy individuals had successfully made it to the summit only to perish or suffer significant and permanent harm, (see Beck Weathers), on their way down.

But the facts tell us that this shouldn’t be surprising. A study conducted by Austrian researchers found that while the most common accident in mountain climbing is falling, (no surprise there), what was surprising was that three quarters of these occurred on the way down!

The same holds true in retirement. Think of your approaching retirement as summiting your financial Mount Everest. Taking withdraws from your investments in retirement is like climbing down which requires even more guidance because the mistakes can be costly, and unlike when you are younger, you don’t have the time or income to overcome them. Below I outline the significant dangers and what can be done to avoid them.

Key Takeaways

If retirement is getting to the top of a mountain, climbing down (taking withdraws) requires even more guidance.

Significant market downturns in the few years prior to and/or after retirement will have the greatest impact on how much money you can spend in retirement and how long your money will last.

It’s imperative you employ strategies to mitigate against these events and the bucket strategy is one of them.

Sequence of Returns

In finance we have a term called “Sequence of Returns” risk. This describes how negative returns in the first years of retirement will have the greatest impact on how long your money will last.

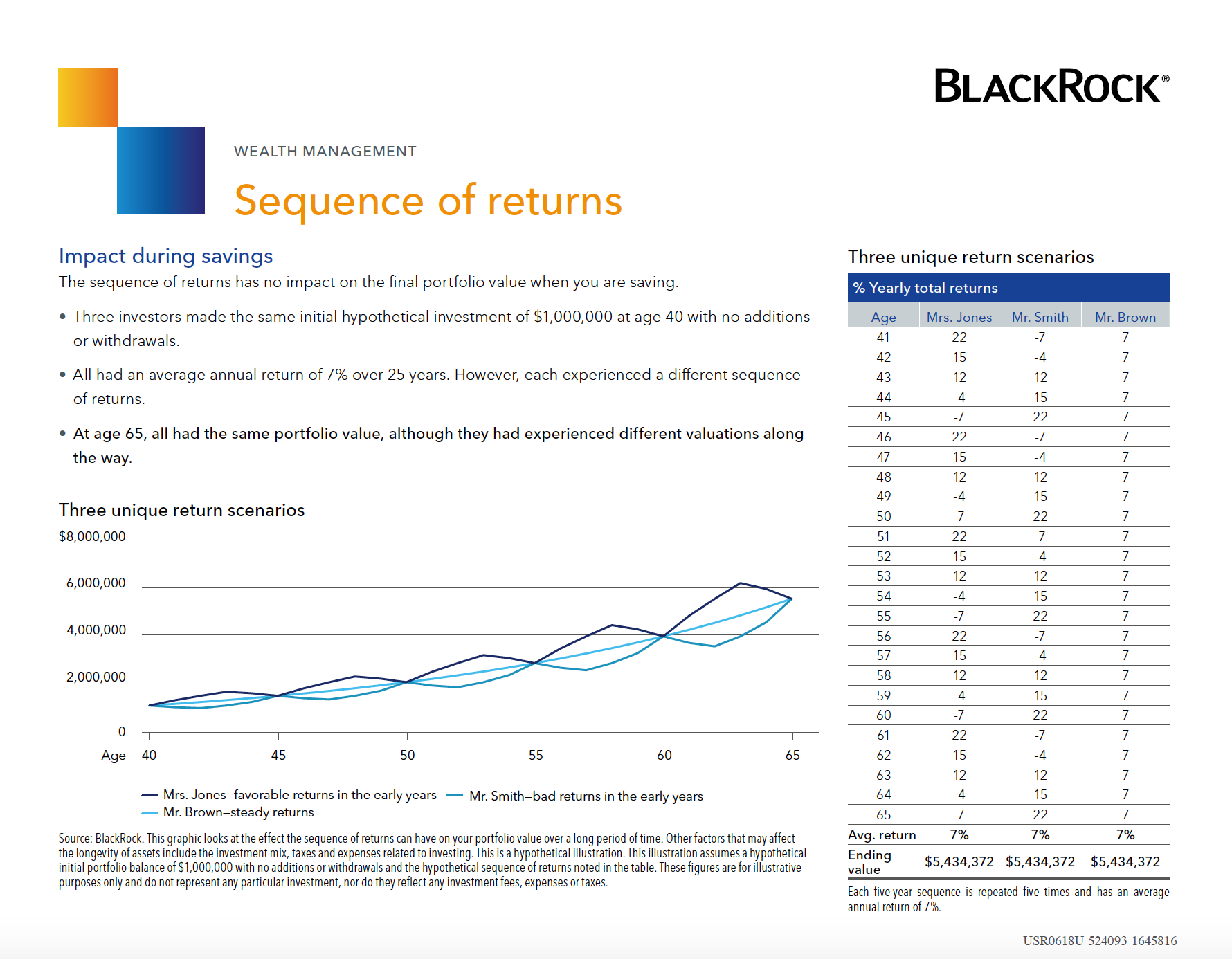

Blackrock Piece on Sequence of Returns

In the image below it goes over the risk of negative returns when you start taking withdrawals. You will see two different hypothetical scenarios for 3 investors. The first hypothetical return shows when investors don’t take withdraws, and the second shows the affect when they do.

Scenario 1 - Each client starts with $1,000,000 at age 40 and make no withdrawals.

“Mrs. Jones” for 5 years has a return of 22%, 15%, 12%, -4%, and -7% for years 1-5 respectively (average annual return is 7%). This exact five year pattern then repeats four more times.

“Mr. Smith” for 5 years has a return of -7%, -4%, 12%, 15%, and 22% for years 1-5 respectively (average annual return is 7%). This exact five year pattern then repeats four more times.

“Mr. Brown” for 5 years has a return of 7%, 7%, 7%, 7%, and 7% for years 1-5 respectively (average annual return is 7%). This five year pattern then repeats four more times.

Outcome for Scenario 1 - At 65 all three investors have the exact same amount because they all averaged a 7% rate of return, and equally important - no withdraws were made.

Scenario 2 - Each client starts with $1,000,000 at age 65 and withdraws $60,000 each year for the next 25 years until age 90.

“Mrs. Doe” started withdraws while earning 22%, 15%, 12%, -4%, and -7%. This pattern is repeated 4 more times. After twenty five years Mrs. Doe still has over a million dollars ($1,099,831) in her account despite withdrawing a total of $1,500,000.

“Mr. White” started withdraws while earning -7%, -4%, 12%, 15%, and 22%. This pattern is repeated 4 more times. Mr. White runs out of money after 23 years at age 88 having withdrawn just over $1,380,000.

“Mr. Rush” started withdraws while earning 7%, 7%, 7%, 7%, and 7%. This pattern is repeated 4 more times. After twenty five years the client still has over $430,020 in their account despite withdrawing a total of $1,500,000.

How can this be?

How do three investors with the same average annual rate of return have such different results? Let’s look at Mrs. Doe: her investments gained 22% that first year. Consequently, her account balance grew to $1,220,000. When she withdrew the $60,000 it only came out of these gains. All her future distributions continued to come out of her gains and consequently her original $1,000,000 was never touched for the entire 25 years of her retirement despite withdrawing over $1,500,000.

Contrast that to Mr. White who lost 7% that first year. His investment decreased $70,000 to $930,000. Once you subtract his annual withdrawal of $60,000 his investments starting in year two were already down to $870,000. The next year his investments were down 4% bringing his balance to $835,200. This coupled with his $60,000 annual withdrawal took his account down to $775,200. Despite the fact that he had three really solid years of returns, 12%, 15%, and 22%, respectively he still ran out of money.

A Single Year Immediately Pre/Post Retirement Can Impact Decades of Spending

This example demonstrates that the rate of return in the first few years of retirement has an enormous impact on whether your money lasts throughout retirement. Just as importantly, the rate of the returns the years prior to retirement are just as critical as well. Ask those who had planned to retire in 2010 when the market cratered in 2009.

It’s just as important in those years as well to take appropriate measures.

So what should you do so you can retire on time and not run out of money during retirement?

Clearly we cannot predict future rates of returns. We don’t know if the stock market will be up 15% or down 10% during the years prior to or during retirement.

Some might think you become very conservative in your investments. However, using the example above if you started with $1,000,000 at age 65 and earned an average rate of return of just 3% and withdrew $60,000/year, you’d still run out of money at 88 years of age.

Introducing the Bucket Strategy

For our clients that are nearing retirement or in retirement we employ a bucket strategy. Essentially, monies that will be withdrawn in the near term, the next 1-5 years are invested more conservatively. Monies that will be withdrawn in the next 6-15 years of retirement are invested moderately. Finally, monies that will be withdrawn in the next 16-25+ years of retirement are invested more aggressively. The ultimate determining factor are the actions of the market, (where we make adjustments), and the individual clients’ spending goals and tolerance for risk.

The logic behind the strategy is that money spent in the near term shouldn’t be impacted by larger swings in the market, and monies that are spent farther in the future are invested to have potential for increased growth to provide future income and offset the effects of inflation (see my blog called The Silent Thief).

We’ve found that clients are far less troubled by fluctuations in the market when they know the monies they will be withdrawing in the near term aren’t affected.

A Sherpa to Help Guide You To and Through Retirement

Certified Financial Planners are the Sherpa’s that guide people through the storms and beautiful weather up and down the mountain. Adjustments will need to be made as you make your way up and down the retirement mountain. There will be life changes, tax code changes, market events, etc. and it’s important to have a guide that understands the changes that are necessary to optimize your unique situation. As the NY Times famous financial sketch artist Carl Richards explains it, “Real Financial Planners are not defenders of outdated maps (financial plans) but rather they are guides in a changing landscape.”

Thank you for taking the time to read this blog, and I hope you found it helpful. If you’d like to discuss your plans to and through retirement, feel free to reach out via the contacts page.

Best Regards,

Jonny West

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

They hypothetical examples listed above are not representative of any specific situation. Your results will vary. The hypothetical rates of return used do not reflect the deduction of fees and charges inherent to investing.

Investing involves risk including loss of principal. No strategy assures success or protects against loss.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful.